Linda McMahon, Secretary of Plunder

Educators are flipping out over Donald Trump’s choice of pro wrestling exec and longtime donor Linda McMahon for secretary of education. Predictably so, since experts in just about every field are flipping out when Trump chooses some poorly qualified (yet very loyal) hack to oversee their specialty—or selects another fox to guard the henhouse.

America’s biggest union, the National Education Association, for instance, slammed McMahon as unqualified and bent on a privatization agenda:

Her chief goal for education is to promote vouchers, which drain resources from public schools and send taxpayer money to unaccountable private schools that are permitted to discriminate against students and educators. The policies she promotes are aligned with Trump’s Project 2025 plan.

McMahon, who served as head of the Small Business Administration during Trump’s initial term, has scant education experience. She earned a teaching certificate in college and was a student teacher for a semester, but resigned from the Connecticut Board of Education in 2010, according to the Washington Post, after the Hartford Courant found that she’d claimed an education degree she never obtained. More recently, a lawsuit accused McMahon and her estranged husband, Vince, of tolerating the sexual abuse of children by an employee of their company, World Wrestling Entertainment. (A lawyer for McMahon told CNN the allegations are “baseless.”)

But hey, she likes vouchers.

Voucher-esque programs, speaking of discrimination, were first deployed across the South during desegregation so authorities could shutter public schools—the white parents didn’t want their kids mixing with Black kids—and instead provide grants to fund the private education of exclusively white children at hundreds of new private schools that popped up to serve them. This was a sordid and horribly racist enterprise, as you will glean from this history compiled by the Center for American Progress.

When states expand voucher programs, shoddy and established school operators both cash in, and public schools and their students are the losers.

And it’s still happening, de facto. ProPublica reported the other day that tens of millions of dollars in public funds are still flowing to these “segregation academies”—of the 39 schools the reporters found in North Carolina alone, more than half had reported to the federal government that their student bodies were at least 85 percent white.

Republicans have been drooling over vouchers for as long as I can remember. They were talking about them when I was in grade school, and I’m a geezer. But now the messaging revolves around school “choice,” with proponents claiming that vouchers, which a number of states have revived in the form of education savings accounts (ESAs), allow low-income parents to escape failing public schools. And this is certainly true to some extent.

But the voucher/ESA cheerleaders neglect to mention that those public schools are failing in significant part because affluent families have fled en masse, and that their budgets have been gutted by, well, the same voucher-loving politicians and/or charter school systems championed by billionaire philanthropists like Bill Gates and the Waltons, and affluent members of both parties. All this drainage leaves many public schools underfunded to the point that teachers literally have to beg for basic classroom supplies—as some did during parents’ night at the public high school my kids attended in Oakland, California.

McMahon or no McMahon, vouchers have come back into vogue recently, likely in reaction to the educational upheaval of the Covid pandemic. “In 2023 alone, seven states passed new school voucher programs and nine expanded existing plans—highlighting a push that is largely coming from red states,” notes a Brookings Institution report published last year.

And sure, some low-income families will benefit from the programs, which channel money that would have gone to the local public school into private accounts (the ESAs) that can be used for private K–12 tuition and related expenses. But there can be a lot of collateral damage, notes the Brookings report.

First, whenever you expand government payouts—and this is something the Republicans complain about in other contexts—fraudsters and opportunists will come out of the woodwork. The report cites research showing that when traditional voucher programs were enacted, a host of “pop-up” private schools would follow, of which many fail quickly. “That’s exactly what is happening with the ESA-style expansions in Arizona now,” the report notes. (Arizona, which in 2011 became the first state to offer ESAs for selected students, expanded its program in 2022 to all students—including those already enrolled in private schools—according to a subsequent Brookings paper that deems the program “a handout to the wealthy.”)

Voucher programs also lead to tuition hikes by existing private schools, according to the Brookings report, “and that is exactly what recent reports are showing with ESA passage.” So, basically, shoddy and established operators alike cash in, and public schools and their students are the big losers.

There are other consequences, too. From the report:

The last decade of research on traditional vouchers strongly suggests they actually lower academic achievement. In Louisiana, for example, two separate research teams found negative academic impacts as high as -0.4 standard deviations—extremely large by education policy standards—with declines that persisted for years. Those results were published across top journals for empirical public and education policy. Similar results in Indiana found impacts closer to -0.15 standard deviations. To put these negative impacts in perspective: Current estimates of COVID-19’s impact on academic trajectories hover around -0.25 standard deviations.

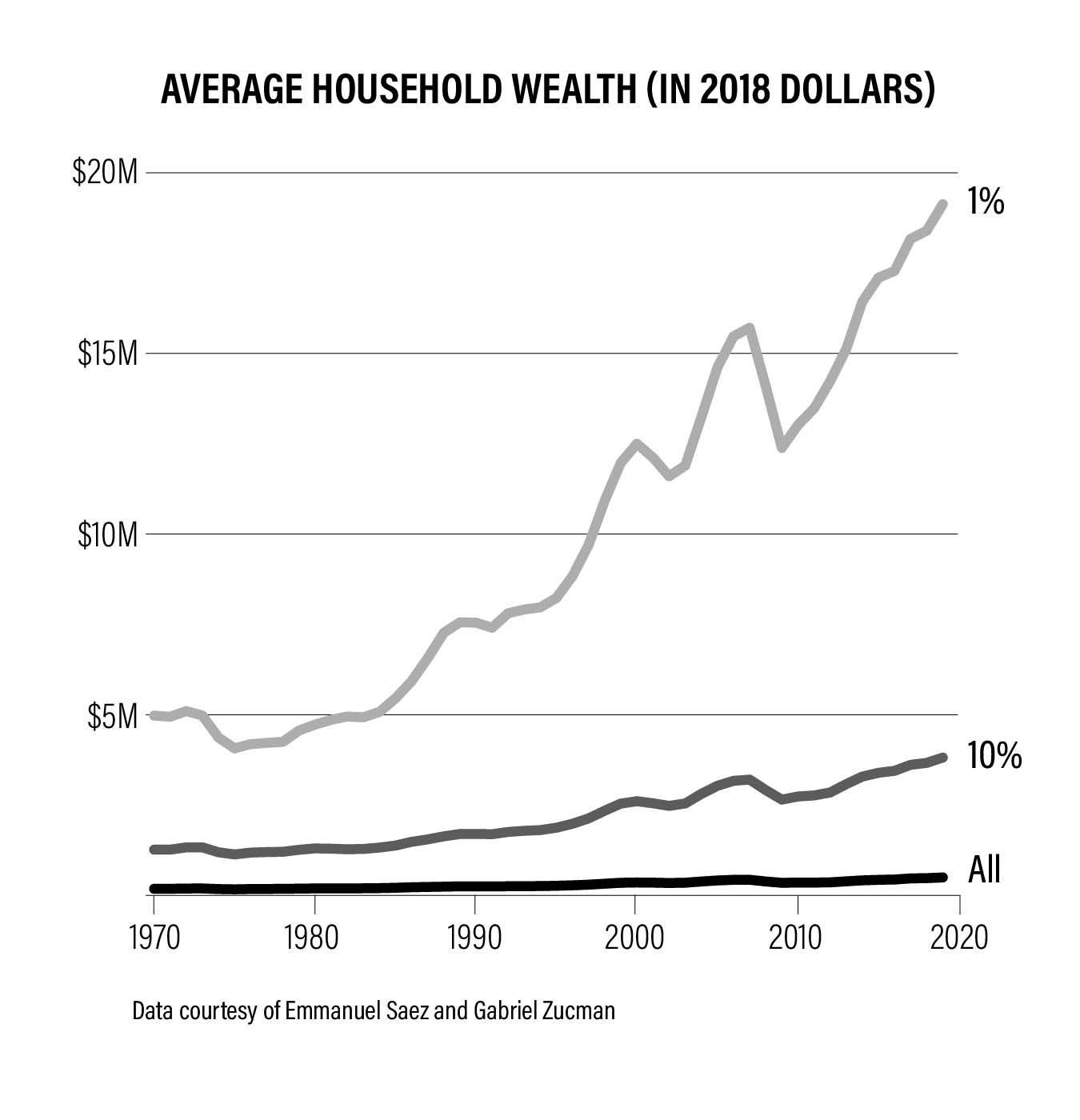

Vouchers, more broadly, are of a piece with what I’ve been calling the Plunder—the steady rigging of our economic system over the past four and a half decades to benefit people who need no government support at the expense of those who really do. This, as I argued in a recent piece, was a primary reason why Trump won a second term, as ironic as that may sound.

I wrote about the rigging of our educational system in my 2021 book about excessive wealth in America. (Chapter title: “Getting In.”) Take the tax-advantaged 529 college savings plans our government offers. Like private retirement plans—401(k)s, IRAs, etc.—these plans provide far more help to rich families than to poor ones. The example I used in my book involved two (fictitious) students living in Ohio, one rich, the other middle-class.

The middle-class family could only afford to put $6,000 a year into their daughter’s 529—an investment fund that grows tax-free over the years and can be used to pay college tuition and qualified expenses when the child comes of age.

And that’s good. They needed that assistance. But for some reason the rules also allow the rich couple in my example to frontload their son’s 529 with up to five years’ worth of the maximum contribution all at once. So, they put $150,000 into a 529 that they set up for him as a newborn, do this again during his fifth year, and then, when he’s 10, bring the balance up to maximum the state allows, beyond which they can contribute no more. With so much cash in their fund from the start, you can imagine how quickly the interest accumulates.

Rich families gained yet another lucrative perk in late 2017, when Donald Trump signed his most notable first-term achievement, the Tax Cuts and Jobs Act. Beyond cutting taxes for wealthy folks and corporations, the TCJA stipulated that parents could now take up to $10,000 a year from their child’s 529 fund for private K–12 tuition. It’s worth noting that elite private high schools—where tuition typically runs between $40,000 to $60,000 a year—offer extensive college admissions mentoring, whereas a middle-class kid at an underfunded public school cannot use their 529 fund to cover expenses like SAT prep, college advising, or essay coaching that their school doesn’t offer in any meaningful way.

When I crunched the numbers, here’s what I found: Even assuming a conservative annual investment return of 5 percent for the students’ 529 funds, the rich family got some $117,000 in tax breaks, nearly seven times what the middle-class family received, not to mention that young Nigel (XTC fans will get the reference) had two and a half years of his private high school tuition covered by the taxpayers. He also ended up with a staggering $688,660 in his fund—likely enough to also cover the cost of law school or med school or business school should he choose any of those paths.

Small wonder that, at the time I reported these numbers, the “Ivy Plus” colleges were enrolling more students from the top-earning 1 percent families than from the bottom 50 percent. And that, compared with kids with families in the bottom 20 percent of the wealth spectrum, the children of 1 percenters were 77 times more likely to attend an Ivy Plus college.

Vouchers only add insult to this injury. They can be marketed to sound like a good and equitable thing—a perk for all Americans—when in reality, without serious means-testing, they end up delivering the most benefit to families who need it the least. They are but one of the levers (here’s another) the Project 2025 people and Trump’s new administration may use to accelerate a plunder that has been in progress for decades, under the watch of both major parties.

One can almost hear it now: the “giant sucking sound” that the late Ross Perot used to talk about, except in this case it won’t be the sounds of US jobs going to Mexico. It will be the sound of the remaining wealth of the middle class getting sucked ever upward and into the coffers of our most privileged.

{kind=link}